Ecosystem Marketplace, an initiative of Forest Trends, is an established source of data and analysis on global environmental finance, markets, and payments for ecosystem services. For nearly two decades, it has offered regular reporting on the state of the voluntary carbon market, becoming a trusted resource for businesses, policymakers, and academics seeking transparency and insights into carbon trading. Its latest publication, the State of the Voluntary Carbon Market 2024, provides a nuanced look at how the market has evolved over the past year amid ongoing debates on quality, integrity, and the future role of carbon dioxide removals (CDR). If you are familiar with our mission at CinSOIL, you know well that we advocate for insetting and believe CDR from carbon farming should not leave the agrifood value chain: insetting means you nurture climate solutions within your own supply chain, rather than buying quick fixes elsewhere. Still, it is extremely important to understand what is happening in the voluntary carbon market so we can leverage emerging best practices, maintain credibility for carbon claims, and ensure that insetting remains a powerful strategy for climate action within the agrifood sector.

The 2024 report reflects a market in flux. On the one hand, total transaction volume and value decreased significantly from the highs of 2022, when concerns about additionality and high-profile critiques of major project methodologies dominated the headlines. This amplified calls for stricter protocols and spurred greater corporate caution toward purchasing offsets, leading to a measured pullback. On the other hand, demand for robust, independently verified carbon credits has not diminished; rather, it is shifting toward higher-integrity projects, including those that directly remove and store atmospheric CO₂. This underscores a growing consensus that CDR, both in engineered solutions like direct air capture and nature-based ones like afforestation, will play an increasingly important role as governments and corporations target net-zero and negative emissions commitments.

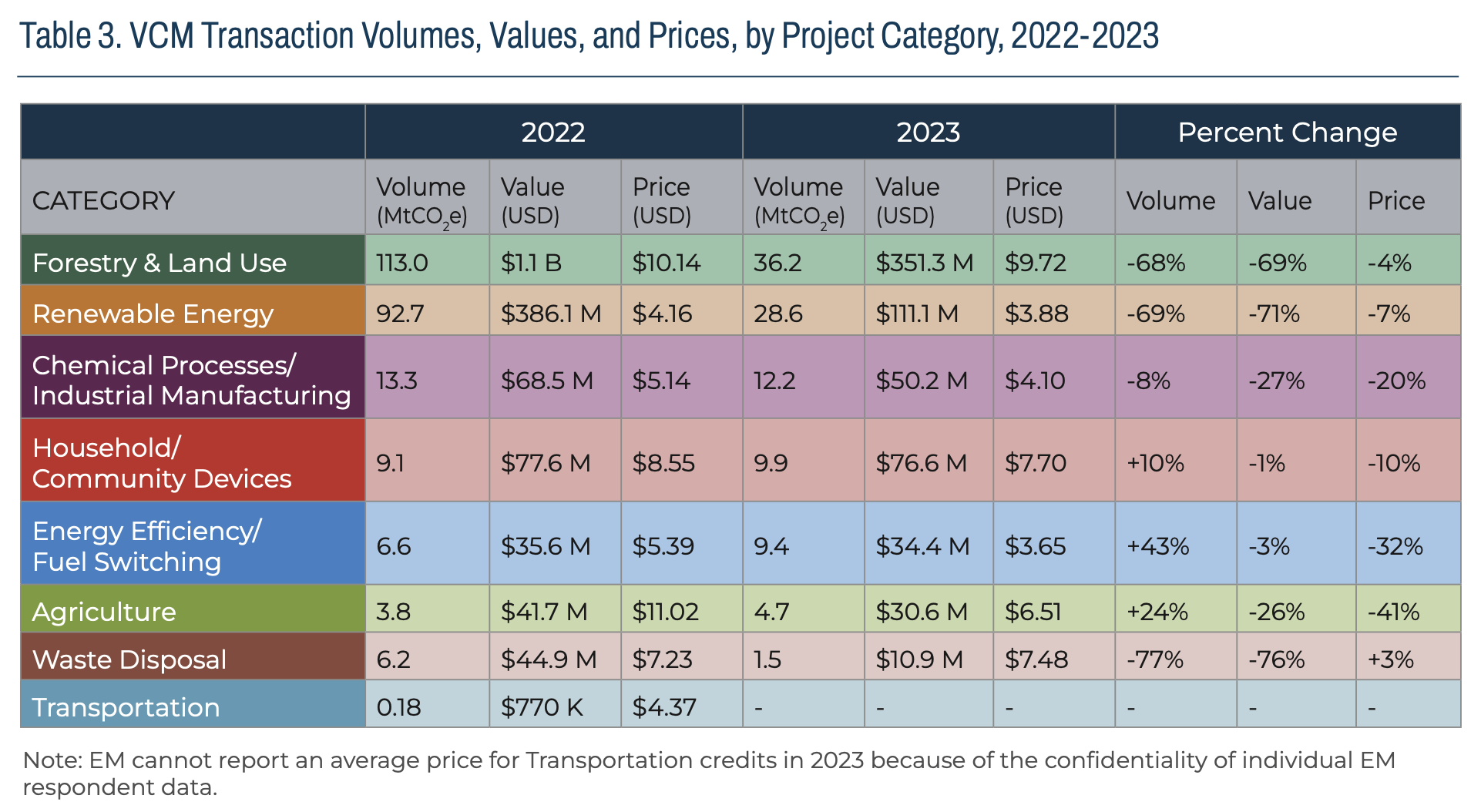

Agriculture, often overlooked in the discourse around carbon markets, receives special attention in the report for its recent momentum. According to the findings, agriculture-based credits witnessed a year-on-year rise in transaction volume, bucking the general downward trend observed elsewhere. This expansion reflects the growing recognition of farmland’s potential to store carbon in soils and biomass. Many of these projects entail regenerative farming or improved grazing systems that enhance soil organic carbon and reduce methane emissions, especially in regions such as Asia and Latin America. Buyers frequently perceive these credits as having multiple co-benefits, including improved food security, farmer livelihoods, and biodiversity gains, all while contributing to greenhouse gas mitigation.

Even amid the broader market’s contraction, agriculture CDR showed a 24% jump in volume, signaling a strong enthusiasm for soil-based climate solutions.

Even so, agriculture-based projects have not been immune from the market’s overall cooling in 2023. The price of agricultural credits fell compared to last year, reflecting the broader, industry-wide caution triggered by increased scrutiny of offset quality. This shift does not necessarily signal skepticism toward agriculture’s climate potential, as many corporate buyers remain keen on land-use projects. Instead, it highlights rising demands for transparent measurement, rigorous verification, and certainty about how much carbon is being stored, for how long, and under which conditions.

Across the sector, there is growing recognition that robust benchmarking, uncertainty assessments, and open data governance are critical to elevating trust in soil-based carbon solutions. These are not just theoretical concerns; sound measurements directly impact how quickly agriculture projects can scale and how confident landowners and buyers are in the outcomes. It is in this spirit that methodology updates are being rolled out by various standards. As emerged from the report, agriculture provides a compelling example of how CDR approaches are maturing while simultaneously adapting to tighter quality requirements. As the market moves toward greater standardization, the conversation is no longer simply about buying or selling carbon credits but about ensuring that these transactions lead to verifiable climate impact.

At CinSOIL, we believe these advances are pivotal to delivering credible, long-term carbon sequestration in agriculture. We are developing reliable, science-backed methods to achieve state-of-the-art Measurement, Monitoring, Reporting, and Verification (MMRV). By addressing uncertainties in everything from soil carbon stock changes to the localized effects of different farming practices, these new tools not only strengthen policy frameworks but also bolster market confidence. Ultimately, a combination of rigorous data and farmer-centered designs will make it easier for producers and agrifood companies to embrace insetting, ensuring that carbon farming can be both robust and beneficial across the entire value chain.